Page 1 :

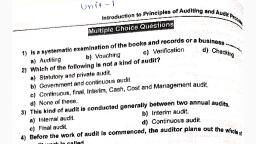

yr, t tect the appropriate io Ss |, i Opti i, 3 n and rewrite the following sentences : at, 4, , The following points should be noted or, , (a) Checking the Voucher ue, (b) Checking the transactions, , (c) Checking the Entry in the Books, (@) Checking existence, Ownership, non, , ked by the auditor in verification of ay, an as, , net, , ° -omission and disclosure, while checking the cut- roc vaune, & off procedures, the Auditor should ensure that, , a) Sales bills are raisi, (a) ed for all goods despatched till the last day of the accounting year, , (b) No sales bills are raised unles', s the Ss were actu: Os, aeounti oa goods were actually despatched and sold during the, , (c) Both the above, (d) None of the above, Auditor should verify stocks which are not lying with the concern c.g. goods on Consignment,, (a) . Through physical verification at consignee’s godown, (b) Through observing the physical verification carried out by the consignee, (c) Byobtaining and examining the confirmation from the consignee, , (d) Byobtaining and examining the confirmation from the consignor, , 4 Closing stock with consignee is to be shown as the asset of, (a) The consignor (b) ‘The consignee, , (c) Both the above (d) None of the above

Page 2 :

© al, , , , , , = ed, : ould be value would, 5. Stock of Goods on Consigament Sh° oa, ( i, (a) Invoice price iowa, (b) Cost or ms arket price W hichever lo" sonsigne® © :, ods were Sent f° the ; whic, (c) Price at which gooes fine amount SEISAH TERE, (d) None of the above . than the outstane (a), 6. Ifthe market value of the security IS ae ‘and advances (o), (a) Difference should be show? as toa tiabilitY whe, (b) Difference should be shown 35 eT ed fai 18 feco, S unsec!, (c) Difference s should be show? as act to known as @), (d) None of the above fer of Prope erty ©), 7 A mortgage duly registered und der the Trans i. sews mortgage oO, (a) Equitable mortgage ae pledge 19 put, i ( with the lender as securit, (c) Hypothecation deeds of the property y. @), S involves si le dee tgage, 8. involves depositing the tit Legal mor :, (b) (, (a) Equitable mortgage w) pledge nN, (c) Hypothecation Ltd. are in the custc ‘ody of a Holding Corpora, 4, . C Ltd. © stment by, 9. Equity shares of XY Ltd. held by AB ify this inves, India Limited (SHCIL). The auditor many yeri (t, Ss., (a) Reviewing last year's orking PaPe™ official of the ABC Ltd. «, (b) Obtaining ® certificate from @ responsib e (, (c) Obtaininga certificate from Se :, ini from XY Lt if, (d) Obtaining a certificate pyaiel savento with book stock, an auditor —, 10. While reconciling a client’s annua own in the book ‘al, cc) ik in hand Was more than that sh s. This ea, , ta, , that for certain items the stoc:, the result of the client’s failur, , Purchase returns, (d), , eto recor, " ) Sales returns, Purchase discounts, , , , , (a), (c) Goods with consignor, Goods Received Notes support entries in, (a) Sales book and sales return book (b) Purchase book and sales return book, (c) Cash book and purchase book (@) Sales book and purchase return book, Which of the following assets cannot be subjected to physical verification 2B., (a) Debtors (b) Land, (c) Building (d) Machinery, The overall objective in the audit of creditors is to determine whether balance of creditors, is overstated, , (a) _ is fairly stated and properly disclosed (b), (d) is accurately stated, , (c) isunderstated, The main focus taken by the auditor in verifying liability balances is on the discovery of, , (1) Understated liabilities, , (11) Omitted liabilities, (a) Lonly (b) only, , - aa rca Wl — (d) Neither L nor I, ich of the following is most reliable for verifying the correct balance of creditels, Supplier's invoices "6 _, , (b) Supplier's statements, , (a), Confirmations ., (ad) Bills of lading, , (¢)

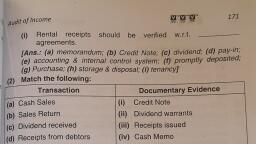

Page 5 :

Dene gy seats, , (Positive, , , , |, (st 253 ie, SAGs Sho, , ceou: ld be / « \, eo es “Should not be deducted) trem the Y, , the M Of con, , bo. Ne bal, Ce sh n Mation the, wit OSitive) p shown, the debtor is asked to write back, = 8 the bal. ©) form of, — Slance ¢ CORKS, fOr CON firmatio, © Shown M tinny,, , , , nei AS Sho,, a Gaditor client) Shouig, , Nation, the de, the debtor is asked to write back only, Feturned to, , , , , , , the, —— (auditor / client) and not to the, , , , Right Shares, , , , , , , , , , , , , , , * onus Shar,, = ie s * 8) Confirmation, ) Debtors &) Add cost to the cost of original shares, © eine of machinery ¢ (c) Certificate from Chartered Engineer, a” ¥ fabricated by (4) Check Title Deeds deposited with, a i lender or solicitor, 6 Loan secured by Legal Mort (e), , Check Mortgage Deed, , Add only no. of shares received to, the number of original shares, Certificate from Civil Contractor, Treat as contingent liability, , () Physical Verification, , j) Certificate from Factory Manager, , Immovable Property, - Lean secured by Equi, , and €xamining evidence in respect of an item of revenue or, qfirmation means obtaining written evidence from management regarding existence of an, at or liability., , involves obtaining and exa:, , mining evidence in respect of an item ofasset or liability, inning of the year., , i f the, balance of the stock book for the next year should be the closing stock 0, ar as per the physical inventory., , stocks are overvalued the profits and assets will be overstated., , re valued at the market price as at the year end., , -ecjation is to be provided on the investments annually., , g the yea o adjustment show dbe nade to the cost of, ived during the y : ‘ : 1 r averag, er O. shares should be incre sed resi Iti g, , nD a ulting in a lower ave! c, , , , ‘ P, | s is valued at c St, 1 ry pi, ane ost, even fthe subsidia com) any has incurred, , , , cnase ac erie: o the date of co pletio 0 th project, 1 S$ up h ym nm f, urchase e, , ost of the machineries.

Learn better on this topic

Learn better on this topic