Notes of Class 11, Accountancy Incomplete Record - Study Material

Page 1 :

e there is NO such, ords’ refer to maintaining, , her words, under the incomplete records, intained which, , g records, , cords’. Sometimes, it i, ry’ becaus|, , “incomplete rec, , of only those records W!, some of the subsidiary pooks and some ledger a, otherwise are ess! der the do’, According to Carter :— ‘, “Single Entry system is a method or a variety of methods, employed for the, the two-fold aspect and consequently fails to, , recording of transactions, which ignore, nessman with the information necessary for him to be able to ascertai, in, , provide the busi, the position.””, , Kohler defines it as :—, “A system of book-keeping i :, eping in which, as a rule, only records of, i ords of cash ai, nd of, , personal accounts are maintai, . *, . ain si i, varying with circumstances,” ed; it is always incomplete doubl, . ouble ent, ry system., ‘9, , ential un, , Salient Features

Page 2 :

ACCOUNTS FROM INCOMPLETE RECORDS, , (2) Maintenance of Cash Book : A Cash Book is maintained under this system, which usually mixes up business as well as private transactions of the proprietor,, , (3) Dependence on Original Vouchers : In order to collect the Tequireg, information one has to depend on original vouchers. For example, the figure of, purchase at the end of a particular period is ascertained by totalling the Original, , " invoices received from the suppliers. Similarly, the figure of sale is ascertained b, , making a total of the copies of invoices which have been issued to the customers, during the year., , (4) Lack of Uniformity : The books maintained under the system may differ from, firm to firm because the system is only an adjustment of double entry system according, to the actual needs and conveniences of the business houses., , (5) Suitability : Books according to this system can be maintained only by a sole, trader or partnership firm. Limited companies cannot keep their books on this system, because of legal provisions., , (6) Preparation of Final Accounts : Since a record of all the nominal and real, accounts is not maintained under this system, the final accounts cannot be prepared, easily. Final accounts can be prepared only after converting the available information, into double entry records and after ascertaining the missing figures. Even then the, figures of assets and liabilities will be based merely on estimates. Because of this, reason the statement of assets and liabilities prepared under this system is termed as, ‘Statement of Affairs’ instead of ‘Balance Sheet’., , Uses or Reasons for keeping Incomplete Records :, , (1) Simple Method : It is an easy and simple method of recording business, transactions because it does not require any special knowledge of the principles of, double entry system., , (2) Less Expensive : Only the cash book and some of the ledger accounts are, maintained under this system. As such, the staff required for maintaining the accounts, is also less in comparison to double entry system., , (3) Suitable for small concerns : This method is most suitable to small business, concerns which have mostly cash transactions and very few assets and liabilities., , ; (4) Easy to calculate profit or loss : It is easier to calculate profit or loss under, this method. For this purpose, only the closing capital has to be compared with the, opening capital along with some adjustments., , (5) Flexible Method : The system is more practical and rejects the strict rules of, , double entry system. It can be easily changed and adjusted according to the needs of, particular business,, , Defects or Limitations of Keeping Incomplete Records ‘, ts (1) Preparation of Trial Balance not possible : The method does not record both, © aspects ofa transaction, As such, a trial balance cannot be prepared to check the, , aeltintetieal accuracy of the books of accounts. This increases the possibility of frauds, and misappropriations,, , (2), Incomplete and Unscientific System : The system is incomplete ee, , urscientitic due to vhe fac: that both the aspects, debit and credit of a.transaction, , Ne ced Ale 5] oe . y, flor recorded Also, ro det rules are fallawed under thie methand 42 224, , , , , , |, |, |, |

Page 3 :

y, , 1S FROM INCOMPLETE REC, ccouN ORDS 993, , A, (3) True Profit or Loss cannot be ascert, , ot maintained, a Trading and Profit, the profit earned or loss suffered dur, , reasonable accuracy., , iffic' Ity i " ., eee Tune sie Paring Balance Sheet : Since real accounts are not, ee Only a ee ecurenarad to depict the true financial position of, the aaa | of affairs is prepared wherei of assets and, jabilities is written on estimated basis. prep: herein the value, (5) No Control on Assets : Since real accounts are not maintained, it is not, , possible to keep full control on the assets and as such, the chances of misappropriation, ofassets cannot be avoided., , ari ained : Because nominal accounts ate, and Loss Account cannot be prepared and hence,, ing a particular period cannot be ascertained with, , (6) No recognition in the assessment of Income Tax and Sales Tax : The system, fails to reveal the true profit and sales of a business. As such, the accounts maintained, under the system are not accepted by tax authorities., , (7) Unsuitable for Planning and Control : The system fails to provide the, adequate and reliable figures required for planning and sound decision-making., , (8) Difficulty in Comparative Study : Due to incomplete information, the, profitability and the financial position of the current year cannot be compared with that, of the previous year and as such, it becomes quite difficult to know the reasons of, improving or deteriorating profitability and financial position of the business., , (9) Proper valuation of assets not possible at the time of sale of business : It, becomes very difficult to fix the correct price of assets, specially goodwill, at the time, of sale of the business., , (10) Internal Check not possible : Because of lack of double entry principles,, internal checking is not possible and hence there are always the chances of errors and, frauds, Also, it becomes very difficult to detect them., , Due to the above mentioned defects the system is known as incomplete,, unscientific and unreliable., ble Entry System and Incomplete Records, , , , , Difference between Dou, , , , Under this system, both the, aspects of very few transactions |, are recorded. For some other,, transactions one aspect and yet), for others no aspect at all is., recorded: s, Only personal accounts: and’, , cash book are maintained un, it. a, , , , , , , , th the aspects of every, transaction are recorded in it., , , , |, , , , , , , W accounts — personal, real, nominal. are maintained

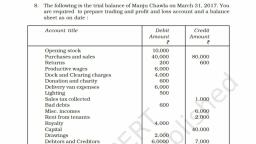

Page 4 :

—, - PUSTRATION 2., Aman started a business on Ist April 2008, with a Capital of 74,50,000. During the, , ear he withdrew 80,000 for household expenses and introduced %14,000 as fresh, Capital. His position of assets and liabilities as at 31st March 2009 stood as follows :, , , , , , , ‘Cash in Hand, , \pills Receivable, , ‘Debtors, , | Creditors, , Bills Payable us, You are required to prepare statement of profit or loss for the ye, , March 2009., , ———, SOLUTION : STATEMENT OF AFFAIRS, as at 31st March 2009, , (Delhi 2010), , , , , , , , , , , , , Geditors. Cash in Hand, , Bills Payable - 5,000 | Stock 0, , ‘Capital (Balancing figure) 000 | Bills Receivable 50,000,, , i | Debtors 8,00,000), , be “000 9,27,000,, = Soe ‘, , , , , , STATEMENT OF PROFIT OR LOSS, for the year ended 31st March 2009, , , , , , , , , , , , , , , , [Gaia as on st March 2009, : Drawings (Household expenses), , , , , , , , , , , , - pasudy t ST ae hes, ILLUSTRATION 3., , pelts Priyanka runs a small Bakery Business. She was not maintaining her, accounts un the dovble entry system. On April 01, 2008 she had started the business, , ao eae ¢ fe mp OT ., 4 Céipitel of 278-006. Ga March 31. 2009 her incomplete records eculd provide >, , , , wants

Learn better on this topic

Learn better on this topic