Notes of 11, Accountancy bills of exchange.pdf - Study Material

Page 1 :

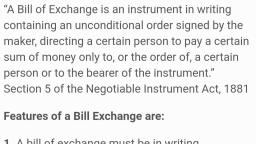

Bills of Exchange, , , , , , , , , , , , , , , , , , , , , , , , , , es, Parties and Specimen of Bills of Exchange ~, , Parties and Specimen of Promissory Note, etween Bill of Exchange and Promissory Note, , Term of Bill, Due Date, Days of Grace, Date of Maturity,, Bill after Date, Bill after Sight ;, , bill before Maturity / Retiring a bill under rebate, ir and Noting of a Bill, , , , BILLS OF EXCHANGE, , ing : In the present era, it is not feasible to run the business exclusively, sh basis. Most of the business transactions take place on credit basis where, buyer of the goods promises to pay the amount after a specified period., ever, the seller of goods desires to have a written undertaking from the, Be payment be made to him on a fix date so that no dispute may take, ata later date. Thus, seller of goods prepares a document containing terms, ‘conditions of sale viz.,. amount to be paid, date and place of payment, etc., ‘buyer of the goods signs on this document to affirm that he has accepted, le terms and conditions laid down. This written document is called as ‘Bill of, ange’. It facilitates the credit sales of goods. In pps /V! this document, ‘Hundi’ and it is written in varlons regional anguages, however, in, , ‘ hese credit instruments are termed as ‘Bill of Exchange’, ee ‘These instruments are governed by Indian Negotiable, , missory ., , ument Act, 1881 in our country:, , Exchange wi \, finition of Bill of ent in writing containing an unconed:, , ve instrum, Bill of Exchange wan uF ertain person to pay a certain sum money, by the maker, directing 4 ah the bearer of the instrument®, oa q, , az: is ”, order of a certain perso" °" "tion 5, Negotiable

Page 2 :

15.2 Accountancy _ 4, , Features or Characteristics of Bill of Exchange, (i) A bill of exchange is a written document., (ii) Tt must contain an order to make the payment., (iti) The order must be unconditional., (iv) It is written and signed by the maker i.c., drawer of the bill., (o) The amount must be specified., (vi) It must be signed by the acceptor of the bill ie, drawee., (vii) The amount of the bill is either payable on demand or on a fixed date, viti) It bears a stamp as per Indian Stamp Act., (ix) The payment of the bill is paid either to the bearer or to drawer or toa, specified person., Parties to a Bill of Exchange, A Bill of Exchange has the following three parties :, (1) Drawer : A bill is written by the seller of goods on the buyer of the, , goods. He is known as drawer of the bill. It contains the amount, date of payment, _, place of payment, etc. and it is also signed by the drawer., , (2) Drawee or Acceptor : The bill is written by the seller on the buyer of, goods. The buyer is liable to make the payment of the bill so he writes the word., “Accepted” on the bill and puts his signature. Thus, he becomes the acceptor of, the bill or drawee of the bill., , (3) Payee : The person who gets the payment of the bill is called payee. (i) If, the drawer retains the bill with himself till the maturity of the bill and gets its, payment, he is payee. (ii) If the bill of exchange is discounted by the drawer,, bank will become payee. (iii) If the bill is endorsed to the third party (endorsee),, endorsee will be the payee of the bill. Thus, the payee will be drawer himself,, bank in case of discounting of bill and endorsee if the bill is endorsed., , Types of Bill of Exchange, From the point of view of accounting, bills of exchange are of two types, (i) Trade Bill ; When bill of exchange is written and drawn for trade, transactions, it is called a trade bill., (ii) Accommodation Bill : When bills are drawn and accepted for mutual, help of both the parties, they are termed as accommodation bill, , , , , , , , , , , , Specimen of a Bill of Exchange, , j Delhi, , 725, 5,000 Nov, 1, 2016, Three. months after date, pay to me or my order, a sum of Rupees ), Stamp | twenty five thousand only, for value received. }, i‘ Ga) :, , Accepted Mohan, , (Sd) ‘ A-41, Naraina Vilur, , Ram Lal New Delhi = 1028, , Gomati Na;, Nagar, , , , , , Here, Mohan is drawer of bill, and Ram Lal is acceptor of the bill.

Page 3 :

dl exchange, 15.3, , s, ages of Bill of Exchange, w Assist in purchase and sale of, eg SN goods on credit :, pill is fixed so the seller of the goods is ee nn el payment, je payment, , } i oa, she bill on the specified date. As suc, : s such, goods can be sold on credit., , gl egal Document : Since bill of excha 21s aw 2 curnent a, n, is ¢ i, a ge is a written docume i, : nt and it is, overed legall from the drawee of the bill if h Is pay, y if he fails to make the payment on, , he due date., (3) Discounting Facility : If the d, : uired to wait ti : drawer of the bill is i, es ioe is the maturity of the bill. He ee need y payment, he, get m the bank before the due date of the bill. eta, , (4) Endorsement of Bill : Bill of, I: hanges i i, I araterred i f exchanges are ne; ‘otiabl, Oo ix Be ae ea oe a settlement e ache ay fe eta, t elieved from makin: :, endorsee will get the payment from the acceptor ane die Le <, e., , (5) No need to send remind:, ers : The seller is relieved i i, tothe buyer of goods to make the payment in meee ce Sena, is, , , , , , , , , , , , , , , , , , (6) Assists in cash i é, ( planning : The seller of goods i, receipt of payment of the bill so he can plan his cn penwitaegs Ree, , (7) Useful in making ! i i, , , g foreign payment : Bill of Exchan, in, o ge may be inland o:, , foreign. Thus, they are also used to promote foreign sale of goods oct ma, , , , , , (8) Provides conveni, , z ience to buyer of goods : The buyer of ;, , . of exchange and thus, gets time to make the pee of auras, , to sell the goods in the mean while. Thus, he can easily make the payne, lymen, , of the bill on its due date., , @ PROMISSORY NOTE, , Often, the bu s giv sae, , : yer Gf goods gives an um ertaking to the seller of, , make the payment of a specified Zmount to the seller, Ox to tus OS er tae Specified, Person, such undertaking of the buyer of goods is called a promissory note., , Definition of Promissory Note, , A promissory note isan instrument in writing (not being a bank note or a curren, Note) containing an unconditional undertaking signed by the maker to pay a certain soi, % money only to or to the order of @ certain person or to the bearer of the instrument, , , , , , , , , , , , _ section 4 of Negotiable Instrument Act, 1881, , ory Note, a certain sum of money., , , , of Promiss, , , , Features or Characteristic®, (i) It is a written undertaking ' pay, , (ii) The undertaking ™ fition’, (iii) It must be signed by, (iv) It specifies the name ol t !, , (v) Specified amount 18 payable, , the bearer., mped as pel, , (vi) It must be 4, , , , ust be uncone, its maker (buyer of goods)., , he payee (receiver of money),, , to the specified person or to his order or Ry, , , , , , , , + its value: ‘eq, ~5a

Page 5 :

=, , go of ronan” 1515, , DUE DATE (DATE OF MATURITY ) AND DAYS OF GRACE, , date / date of maturity is the date on which the payment of bill is due., piscaleulated by adding 3 days to the period of the bill and it is called days of, , ea for Calculating Due Date / Maturity Date of a bill :, (i) No days of grace are added to ‘demand bill’ or ‘at sight bill’., (i) When period of bill is given in months : The maturity date will be, calculated in terms of calender months (ignoring the number of days in, a month) but 3 days of grace are added., , (ii) When period of bill is given in days : Maturity date will be calculated, in days after adding 3 days of grace (excludes date of transaction but, includes date of payment). i, Example : A bill is drawn on Ist January, 2017 payable after 60 days. Its, due date will be after 63 (60+3 days of grace) days i.e., March 5, 2010, (ie., 30 days of January + 28 days of February + 5 days of March)., , (iz) If maturity date becomes a public holiday : The maturity date of the, bill shall be 1 day prior to due date., , Example : A bill is drawn on 12 June for 2 months. Its due date comes to, 15th August which is a national holiday so its due date becomes 14th, August ie., 1 day prior to its due date., , (2) If maturity date is declared as ‘emergency holiday’ which has not been, declared holiday earlier, the due date shall be after 1 days from date of, maturity., Example :, on 4 March (i.e.,, as holiday by the gove”, the due date)., , ILLUSTRATION 1. Calculate, , A bill is drawn for 2 months on Ist January, its due date falls, 2 months + 3 days of grace) but if March 4 is declared, nment, its date will be March 5 (i.e, 1 day after, , the due date of the bill in the following cases ;, Period, , Date of Bill 2 months, (i) 1st January, 2017 1 month, (ii) 30th January, 2016 1 month, (iti) 31st January, oa 1 month, . ae 2015 Gren, v, y ", (vi) 30th June, 201° 60 ae, (vii) 1st July, 2016 2 months, (viii) 12th Janey a 2016 2 months, (ix) 23rd NovernDe” 30 days,, (x) 13th July, 206 ny aac 5, SOLUTION: 2017 iv) a V2016, (i) 4th March, March, 2016, , 2016, , (ii) 3rd Marehy >

Learn better on this topic

Learn better on this topic