Notes of BTech Sem-I 2021-22, Financial Management Notes Unit 5 FM.pdf - Study Material

Page 1 :

Financial Management BTech ENTC Engg., , UNIT - 5, Time Value of Money & Capital Budgeting: Concept of time value of money,, , Compounding & discounting; Future value of single amount & annuity, present value of, single amount & annuity; Practical application of time value technique. Capital, budgeting - Nature and significance, techniques of capital budgeting -Pay Back Method,, Accounting rate of return, Internal Rate of Return, DCF, Net Present Value and, profitability index., , , , , , 1. Concept of time value of money:, , The time value of money (TVM) is the concept that a sum of money is worth more now, than the same sum will be at a future date due to its earnings potential in the interim., , This is a core principle of finance. A sum of money in the hand has greater value than, the same sum to be paid in the future., , The time value of money is also referred to as present discounted value., , ¢ Time value of money means that a sum of money is worth more now than the, same sum of money in the future., , e This is because money can grow only through investing. An investment delayed, is an opportunity lost., , e The formula for computing the time value of money considers the amount of, money, its future value, the amount it can earn, and the time frame., , « For savings accounts, the number of compounding periods is an important, determinant as well., , e Formula for Time Value of Money, , Depending on the exact situation, the formula for the time value of money may change, slightly. For example, in the case of annuity or perpetuity payments, the generalized, formula has additional or fewer factors. But in general, the most fundamental TVM, formula takes into account the following variables:, , FV = Future value of money, , PV = Present value of money, , i = interest rate, , n= number of compounding periods per year, t= number of years, , Based on these variables, the formula for TVM is:, , FV=PVx[1+(i/n)]%", , Prepared by Prof. Shaikh R P, ENTC Dept.

Page 2 :

Financial Management BTech ENTC Engg., , e¢ Components of TVM, The key components are as mentioned below —, , 1. Interest/Discount Rate (i)- It's the rate of discounting or compounding that we apply, to an amount of money to calculate its present or future value., , 2. Time Periods (n) — It refers to the whole number of time periods for which we want to, calculate the present or future value of a sum. These time periods can be annually, semi, -annually, quarterly, monthly, weekly, etc., , 3. Present value (PV)- The amount of money that we obtain by applying a discounting, rate on the future value of any cash flow., , 4. Future value (FV)- The amount of money that we obtain by applying a compounding, rate on the present value of any cash flow., , 5. Installments (PMT)- Installments represent payments to be paid periodically or, received during each period. The value is positive when payments have been received, and become negative when payments are made., , 2. Difference Between Compounding and Discounting, , Time Value of Money says that the worth of a unit of money is going to be changed in, future. Put simply, the value of one rupee today will be decreased in future. The whole, concept is about the present value and future value of money. There are two methods, used for ascertaining the worth of money at different points of time, namely,, compounding and discounting. Compounding method is used to know the future value, of present money. Conversely, discounting is a way to compute the present value of, future money., , , , BASIS FOR, , COMPARISON COMPOUNDING DISCOUNTING, , Meaning The method used to determine the The method used to determine the, future value of present investment is present value of future cash flows, known as Compounding. is known as Discounting., , Concept If we invest some money today, what What should be the amount we, will be the amount we get at a future need to invest today, to get a, date. specific amount in future., , Use of Compound interest rate. Discount rate, , Prepared by Prof. Shaikh R P, ENTC Dept.

Page 3 :

Financial Management BTech ENTC Engg., , COMPARISON © COMPOUNDING DISCOUNTING, , Known Present Value Future Value, , Factor Future Value Factor or Compounding Present Value Factor, Factor Discounting Factor, , Formula FV =PV(14+1r)‘n PV=FV/(1+r)4n, , e Definition of Compounding, , For understanding the concept of compounding, first of all, you need to know about the, term future value. The money you invest today, will grow and earn interest on it, after a, certain period, which will automatically change its value in future. So the worth of the, investment in future is known as its Future Value. Compounding refers to the process of, earning interest on both the principal amount, as well as accrued interest by reinvesting, the entire amount to generate more interest., , Compounding is the method used in finding out the future value of the present, investment. The future value can be computed by applying the compound interest, formula which is as under:, , Future Value:, , Single Cash Flow = Amount (1+R)", , ([Q+R)®— 1], , Annuity = Amount X z, , Where n = number of years, R = Rate of return on investment., , ¢ Definition of Discounting, , Discounting is the process of converting the future amount into its Present Value. Now, you may wonder what is the present value? The current value of the given future value is, known as Present Value. The discounting technique helps to ascertain the present value, of future cash flows by applying a discount rate. The following formula is used to know, the present value of a future sum:, , Prepared by Prof. Shaikh R P, ENTC Dept., , or

Page 4 :

Financial Management BTech ENTC Engg., , FV; FV, FV;, , Present Value = —— + —— + —— +, (1+R)! (4+R)2 (1+R)?, , , , Where 1,2,3......9 represents future years, FV = Cash flows generated in different years,, R = Discount Rate, , For calculating the present value of single cash flow and annuity the following formula, should be used:, , Present Value:, , 2 Li, Single Cash Flow = Amount X ————, (14+R)2, , [G+R)"—- 1], , Annuity = Amount X, R(i+R)®, Where R = Discount Rate, , n = number of years, , e Key Differences Between Compounding and Discounting, The following are the major differences between compounding and discounting:, , 1. The method uses to know the future value of a present amount is known as, Compounding. The process of determining the present value of the amount to, be received in the future is known as Discounting., , 2. Compounding uses compound interest rates while discount rates are used in, Discounting., , 3. Compounding of a present amount means what will we get tomorrow if we, invest a certain sum today. Discounting of future sum means, what should we, need to invest today to get the specified amount tomorrow., , 4. The future value factor table is referred to calculate the future value in case of, compounding. Conversely, in discounting, present value can be computed with, the help of a Present value factor table., , 5. In compounding, present value amount is already specified. On the other hand,, the future value is given in the case of discounting., , Prepared by Prof. Shaikh R P, ENTC Dept.

Page 5 :

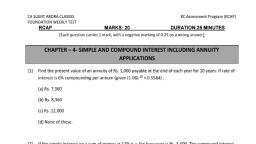

Financial Management BTech ENTC Engg., , Present Value:, , 1. Present Value of a Future Sum:, The present value formula is the core formula for the time value of money; each, of the other formulae is derived from this formula., , For example- the annuity formula is the sum of a series of present value, calculations., , The Present Value (PV) formula has four variables, each of which can be solved for, , Va FV, (1+i)", * PVis the value at time=0, ¢ FV is the value at time=n, * iis the rate at which the amount will be compounded, each period, ¢ nis the number of periods, The cumulative present value of future cash flows can be, calculated by summing the contributions of FV,, the value of, cash flow at time=t, , , , n, Pv=)" a t, t-9 (1 +i) :, Note that this series can be summed for a given value of, n, or when n iso. This is a very general formula, which leads, to several important special cases., , 2. Present Value of an Annuity for n Payment Periods:, , In this case the cash flow values remain the same throughout the n periods. The, present value of an annuity formula has four variables, each of which can be solved, for , , , viaje’ li I, i (i+i)", ¢ PV(A) is the value of the annuity at time=0, ¢ A is the value of the individual payments in each, compounding period, ¢ i equals the interest rate that would be compounded, for each period of time, ¢ nis the number of payment periods., To get the PV of an annuity due, multiply the equation, by (1 + i)., , Prepared by Prof. Shaikh R P, ENTC Dept.

Learn better on this topic

Learn better on this topic