Notes of B.com III, Costing I & II Unit 1. Introduction to Cost Accounting - Study Material

Page 1 :

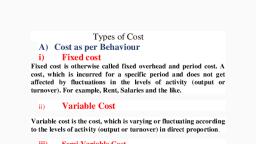

Unit 1. INTRODUCTION TO COST ACCOUNTING, DEFINITION, SCOPE, OBJECTIVES AND SIGNIFICANCE OF COST ACCOUNTING, ITS RELATIONSHIP WITH FINANCIAL ACCOUNTING AND MANAGEMENT ACCOUNTING, Way back to 15th Century, no accounting system was there and it was the barter system prevailed. It was in the last years of 15th century Luca Pacioli, an Italian found out the double entry system of accounting in the year 1494. Later it was developed in England and all over the world up to 20th Century. During these 400 years, the purpose of Cost Accounting needs are served as a small branch of Financial Accounting except a few like Royal wallpaper manufactory in France (17th Century), and some iron masters & potters (18th century)., The period 1880 AD- 1925 AD saw the development of complex product designs and the emergence of multi activity diversified corporations like Du Pont, General Motors etc. It was during this period that scientific management was developed which led the accountants to convert physical standards into Cost Standards, the latter being used for variance analysis and control., During the World War I and II the social importance of Cost Accounting grew with the growth of each country’s defence expenditure. In the absence of competitive markets for most of the material required for war, the governments in several countries placed cost-plus contracts under which the price to be paid was cost of production plus an agreed rate of profit. The reliance on cost estimation by parties to defence contracts continued after World War II., In addition to the above, the following factors have made accountants to find new techniques to serve the industry:, Limitations placed on financial accounting, i) Improved cost consciousness, (ii) Rapid industrial development after industrial revolution and world wars, (iii) Growing competition among the manufacturers, (iv) To control galloping price rise, the cost of computing the precise cost of product / service, (v) To control cost several legislations passed throughout the world and India too such as Essential Commodities Act, Industrial Development and Regulation Act...etc, Due to the above factors, the Cost Accounting has emerged as a specialized discipline from the initial years of 20th century i.e after World War I and II., In India, prior to independence, there were a few Cost Accountants, and they were qualified mainly from I.C.M.A. (now CIMA) London. During the Second World War, the need for developing the profession in the country was felt, and the leadership of forming an Indian Institute was taken by some members of Defence Services employed at Kolkata. However, with the enactment of the Cost and Works Accountants of India Act, 1959, the Institute of Cost and Works Accountants of India (Now called as The Institute of Cost Accountants of India) was established at Kolkata. The profession assumed further importance in 1968 when the Government of India introduced Cost Audit under section 233(B) of the Companies Act, 1956. At present it is under Section 148 of the Companies Act, 2013., Many times we use Cost Accounting, Costing and Cost Accountancy interchangeably. But there are differences among these terms. As a professional, though we use interchangeably we must know the meaning of each term precisely., Cost Accounting: Cost Accounting may be defined as “Accounting for costs classification and analysis of expenditure as will enable the total cost of any particular unit of production to be ascertained with reasonable degree of accuracy and at the same time to disclose exactly how such total cost is constituted”. Thus, Cost Accounting is classifying, recording an appropriate allocation of expenditure for the determination of the costs of products or services, and for the presentation of suitably arranged data for the purpose of control and guidance of management., Cost Accounting can be explained as follows:, Cost Accounting is the process of accounting for cost which begins with recording of income and expenditure and ends with the preparation of statistical data., It is the formal mechanism by means of which cost of products or services are ascertained and controlled., Cost Accounting provides analysis and classification of expenditure as will enable the total cost of any particular unit of product / service to be ascertained with reasonable degree of accuracy and at the same time to disclose exactly how such total cost is constituted. For example, it is not sufficient to know that the cost of one pen is ` 25/- but the management is also interested to know the cost of material used, the amount of labour and other expenses incurred so as to control and reduce its cost., It establishes budgets and standard costs and actual cost of operations, processes, departments or products and the analysis of variances, profitability and social use of funds., Thus, Cost Accounting is a quantitative method that collects, classifies, summarises and interprets information for product costing, operation planning and control and decision making., Cost: 1. ICMA London “ Cost is the amount of expenditure incurred on or attributable to a given thing”., 2. W.M. Harpur “A cost is the value of economic resources used as a result of, producing or doing thing costed”., 3. According to Oxford Dictionary, Cost is “the price paid for something”, Costing : Costing is defined as the technique and process of ascertaining costs. The technique in costing consists of the body of principles and rules for ascertaining the costs of products and services. The technique is dynamic and changes with the change of time. The process of costing is the day to day routine of ascertaining costs. It is popularly known as an arithmetic process. For example, If the cost of producing a product say ` 200/-, then we have to refer material, labour and expenses accounting and arrive the above cost as follows:, Material 100, Labour 40, Expenses 60, Total Rs. 200, Finding out the breakup of the total cost from the recorded data is a daily process. That is why it is called arithmetic process/daily routine. In this process we are classifying the recorded costs and summarizing at each element and total is called technique., Cost Accounting: Cost Accounting means recording of expenditure and income in a systematic way would be useful in arriving at the cost of production, process etc., Weldon defines “Cost accounting is the classifying, recording and appropriate allocation of expenditure for the determination of the costs of products or services, the relation of these costs to sales values and the ascertainment of profitability”., ICMA London defines “Process of accounting for cost from the point at which expenditure is incurred or committed to the establishment of its ultimate relationship with cost centres and cost units. In its widest usage, it embraces the preparation of statistical data, the application of cost control methods and ascertainment of profitability of activities carried out or planned”., Cost Accountancy: Cost Accountancy is defined as ‘the application of Costing and Cost Accounting principles, methods and techniques to the science, art and practice of cost control and the ascertainment of profitability’. It includes the presentation of information derived there from for the purposes of managerial decision making. Thus, Cost Accountancy is the science, art and practice of a Cost Accountant., (a) It is a science because it is a systematic body of knowledge having certain principles which a cost accountant should possess for proper discharge of his responsibilities., (b) It is an art as it requires the ability and skill with which a Cost Accountant is able to apply the principles of Cost Accountancy to various managerial problems., (c) Practice includes the continuous efforts of a Cost Accountant in the field of Cost Accountancy. Such efforts of a Cost Accountant also include the presentation of information for the purpose of managerial decision making and keeping statistical records., Objectives of Cost Accounting, The following are the main objectives of Cost Accounting:, (a) To ascertain the Costs under different situations using different techniques and systems of costing, (b) To determine the selling prices under different circumstances, (c) To determine and control efficiency by setting standards for Materials, Labour and Overheads, (d) To determine the value of closing inventory for preparing financial statements of the concern, (e) To provide a basis for operating policies which may be determination of Cost Volume relationship, whether to close or operate at a loss, whether to manufacture or buy from market, whether to continue the existing method of production or to replace it by a more improved method of production. etc, Scope of Cost Accountancy, The scope of Cost Accountancy is very wide and includes the following:, (a) Cost Ascertainment: The main objective of Cost Accounting is to find out the Cost of product / services rendered with reasonable degree of accuracy., (b) Cost Accounting: It is the process of Accounting for Cost which begins with recording of expenditure and ends with preparation of statistical data., (c) Cost Control: It is the process of regulating the action so as to keep the element of cost within the set parameters., (d) Cost Reports: This is the ultimate function of Cost Accounting. These reports are primarily prepared for use by the management at different levels. Cost reports helps in planning and control, performance appraisal and managerial decision making., (e) Cost Audit: Cost Audit is the verification of correctness of Cost Accounts and check on the adherence to the Cost Accounting plan. Its purpose is not only to ensure the arithmetic accuracy of cost records but also to see the principles and rules have been applied correctly., To appreciate fully the objectives and scope of Cost Accounting, it would be useful to examine the position of Cost Accounting in the broader field of general accounting and other sciences. i.e Financial Accounting, Management Accounting, Engineering and Service Industry., Financial Accounting and Cost Accounting: Financial Accounting is primarily concerned with the preparation of financial statements, which summarise the results of operations for selected period of time and show the financial position of the company at particular dates. In other words Financial Accounting reports on the resources available (Balance Sheet) and what has been accomplished with these resources (Profit and Loss Account). Financial Accounting is mainly concerned with requirements of creditors, shareholders, government, prospective investors and persons outside the management. Financial Accounting is mostly concerned with external reporting., Cost Accounting, as the name implies, is primarily concerned with determination of cost of something, which may be a product, service, a process or an operation according to costing objective management. A cost Accountants primarily charged with the responsibility of providing cost data for whatever purposes they may be required for., The main differences between Financial and Cost Accounting are as follows:, Cost Accounting and Management Accounting:, Management Accounting is primarily concerned with management. It involves application of appropriate techniques and concepts, which help management in establishing a plan for reasonable economic objective. It helps in making rational decisions for accomplishment of these objectives. Any workable concept or techniques whether it is drawn from Cost Accounting, Financial Accounting, Economics, Mathematics and Statistics, can be used in Management Accountancy. The data used in Management Accountancy should satisfy only one broad test. It should serve the purpose that it is intended for. A Management Accountant accumulates, summarizes and analysis the available data and presents it in relation to specific problems, decisions and day-to-day task of management. A Management Accountant reviews all the decisions and analysis from management’s point of view to determine how these decisions and analysis contribute to overall organizational objectives. A Management Accountant judges the relevance and adequacy of available data from management’s point of view., The scope of Management Accounting is broader than the scope of Cost Accountancy. In Cost Accounting, primary emphasis is on cost and it deals with its collection analysis relevance interpretation and presentation for various problems of management. Management Accountancy utilizes the principles and practices of Financial Accounting and Cost Accounting in addition to other management techniques for efficient operations of a company. It widely uses different techniques from various branches of knowledge like Statistics, Mathematics, Economics, Laws and Psychology to assist the management in its task of maximising profits or minimising losses. The main thrust in Management Accountancy is towards determining policy and formulating plans to achieve desired objective of management. Management Accounting makes corporate planning and strategy effective., From the above discussion we may conclude that the Cost Accounting and Management Accounting are interdependent, greatly related and inseparable., Advantages of Cost Accounting:, Cost Accounting has manifold advantages, a summary of which is given below. It is not suggested that having installed a system of Cost Accounting, a concern will expect to derive all the benefits stated here, the nature and the extent of the advantages obtained will depend upon the type, adequacy and efficiency of the cost system installed and the extent to which the various levels of management are prepared to accept and act upon the advice rendered by the cost system., The Cost Accounting System has the following advantages:, (i) A cost system reveals unprofitable activities, losses or inefficiencies occurring in any form such as (a) Wastage of man power, idle time and lost time., (b) Wastage of material in the form of spoilage, excessive scrap etc., and, (c) Wastage of resources, e.g. inadequate utilization of plant, machinery and other facilities., (ii) Cost Accounting locates the exact causes for decrease or increase in the profit or loss of the business. It identifies the unprofitable products or product lines so that these may be eliminated or alternative measures may be taken., (iii) Cost Accounts furnish suitable data and information to the management to serve as guides in making decisions involving financial considerations., (iv) Cost Accounting is useful for price fixation purposes. Although sale price is generally related more to economic conditions prevailing in the market than to cost, the latter serves as a guide to test the adequacy of selling prices., (v) With the application of Standard Costing and Budgetary Control methods, the optimum level of efficiency is set., (vi) Cost comparison helps in cost control. Comparison may be period to period, of the figures in respect of the same unit or factory or of several units in an industry by employing Uniform Costs and Inter- Firm Comparison methods. Comparison may be made in respect of cost of jobs, process or cost centres., (vii) A cost system provides ready figures for use by the Government, wage tribunals and boards, and labour and trade unions., (viii) When a concern is not working to full capacity due to various reasons such as shortage of demands or bottlenecks in production, the cost of idle capacity can readily work out and repealed to the management., (ix) Introduction of a cost reduction programme combined with operations research and value analysis techniques leads to economy., (x) Marginal Costing is employed for suggesting courses of action to be taken. It is a useful tool for the management for making decisions., (xi) Determination of cost centres or responsibility centres to meet the needs of a Cost Accounting system, ensures that the organizational structure of the concern has been properly laid responsibility can be properly defined and fixed on individuals., (xii) Perpetual inventory system which includes a procedure for continuous stock taking is an essential feature of a cost system., (xiii) The operation of a system of cost audit in the organization prevents manipulation and fraud and assists in furnishing correct and reliable cost data to the management as well as to outside parties like shareholders, the consumers and the Government., Limitations of Cost Accounting system:, Like any other system of accounting, Cost Accountancy is not an exact science but an art which has developed through theories and accounting practices based on reasoning and common sense. Many of the theories cannot be proved nor can they be disproved. They grownup in course of time to become conventions and accepted principles of Cost Accounting. These principles are by no means static, they are changing from day to day and what is correct today may not hold true in the circumstances tomorrow., Large number of Conventions, Estimates and Flexible factors: No cost can be said to be exact as they incorporate a large number of conventions, estimations and flexible factors such as-, Classification of costs into its elements., Materials issue pricing based on average or standard costs., Apportionment of overhead expenses and their allocation to cost units/centres., Arbitrary allocation of joint costs., Division of overheads into fixed and variable., Cost Accounting lacks the uniform procedures and formats in preparing the cost information of a product/ service. Keeping in view this limitation, all Cost Accounting results can be taken as mere estimates., Installation of Cost System or Cost Accounting System:, From what has been stated in the preceding sections, it will be seen that there cannot be a readymade cost system suitable for a business. Such system has to be specially designed for an undertaking to meet its specific needs. Before installing a cost system proper care should be taken to study and taken into account all the aspects involved as otherwise the system will be a misfit and full advantages will not be realized from it. The following points should be looked into and the prerequisites satisfied before installing a cost system:, The nature, method and stages of production, the number of varieties and the quantity of each product and such other technical aspects should be examined. It is to be seen how complex or how simple the production methods are and what is the degree of control exercised over them, The size, layout and organisation of the factory should be studied., The methods of purchase, receipt, storage and issue of materials should be examined and modified wherever considered necessary., The wage payment methods should be studied., The requirements of the management and the policy adopted by them towards cost control should be kept in view., The cost of the system to be installed should be considered. It is needless to emphasize that the installation and operation of system should be economic., The system should be simple and easy to operate., The system can be effectively run if it is appropriate and properly suited to the organisation., Forms and records of original entry should be so designed and to involve minimum clerical work and expenditure., The system should be so designed that cost control can be effectively exercised., The system should incorporate suitable procedure for reporting to the various levels of management. This should be based on the principles of exception., COST OBJECT, COST CENTERS AND COST UNIT:, Cost: Cost is a measurement, in monetary terms, of the amount of resources used for the purpose of production of goods or rendering services., Cost in simple, words, means the total of all expenses. Cost is also defined as the amount of expenditure (actual or notional) incurred on or attributable to a given thing or to ascertain the cost of a given thing. Thus, it is that which is given or in sacrificed to obtain something. The cost of an article consists of actual outgoings or ascertained charges incurred in its production and sale. Cost is a generic term and it is always advisable to qualify the word cost to show exactly what it meant, e.g., prime cost, factory cost, etc. Cost is also different from value as cost is measured in terms of money whereas value in terms of usefulness or utility of an article., According to ICMA “Cost unit is a unit of product, service or time in relation to which costs may be ascertained or expressed”, Cost Centres: According to ICMA “Cost centre is a person, location or item of equipment for which cost may be ascertained and used for the purpose of cost control”., Types of Cost Centers:, Production cost center, Service cost centre, Mixed cost centre, Or, Personnel cost centre, Impersonnel cost centre, Cost Unit: ICMA defines “Cost unit of product or service or time in relation to which cost may be ascertained or expressed”., Cost unit is unit of measurement of cost e.g. cost per ton, cost per km. cost per metre, cost per meal etc., Types 1, Single cost unit 2. Composite cost unit

Learn better on this topic

Learn better on this topic