Page 1 :

Cost And Management Accounting, UNIT-1- INTRODUCTION: Meaning and definition of cost, costing, cost, accounting and cost accountancy; objectives, advantages and limitations of, cost accounting, differences between cost accounting and financial, accounting & cost accounting and management accounting. Preparation of, cost sheet and estimation ( problems), , Meaning of Cost Accounting, “Cost accounting is the application of accounting and costing principles,, methods and techniques in the ascertainment of costs and the analysis of saving / or, excess cost incurred as compared with previous experience of with standards’ Thus,, cost accounting relates to the collection, classification, ascertainment of cost and its, accounting the control relating to the various elements of cost. It establishes budgets, and costs and actual cost of operation, process, department of products and the analysis, of variances, profitability and social use of funds, Thus Cost Accounting has the following features :, a. It is process of accounting for costs, b. It records income and expenditure relating to production of goods and services., c. It provides statistical data on the basis of which future estimates are prepared and, quotations are submitted., d. It is concerned with cost ascertainment and cost control, e. It establishes budgets and standards so that actual cost may be compared to find out, deviations or variances, f. It involves the preparation of right information to the right person at the right time, so that it may be helpful to the management for planning, control and decision, making., Cost Accountancy is the application of costing and cost accounting principles., Importance of Cost Accounting, The following are the main objectives of Cost accounting :a. To ascertain the cost per unit of the different products manufactured by a business, concern, b. To provide a correct analysis of cost both by process or operations and by different, elements of cost., c. To disclose sources of wastage whether of material, time of expense or in the use, machinery, equipment and tools and to prepare such reports which may be necessary to, control such wastage., d. To provide requisite data and serve as a guide to price fixing of products manufactured, or services rendered., e. To ascertain the profitability of each of the products and advise management as to how, these profits can be maximized., f. To exercise effective control of stocks of raw materials, work-in-prograss, consumable, stores and finished goods in order to minimize the capital locked up in these stocks.

Page 2 :

g. To reveal sources of economy by installing and implementing a system of cost control, for materials, labour and overhead., h. To advise management on future expansion policies and proposed capital projects., i. To present and interpret data for management planning, decision – making and control., j. To help in the preparation of budgets and implementation of budgetary control., k. To organize an effective information system so that different levels of management, may get the required information at the right time in right form for carrying out their, individual responsibilities in an efficient manners., l. To guide management in the formulation and implementation of incentive bonus plans, based on productivity and cost savings., m. To supply useful data to management for taking various financial decisions such as, introduction of new products, replacement of labour by machine etc., n. To help in supervising the working of punched card accounting or data processing, through computers., o. To organize the internal audit system to ensure effective working of different, departments., p. To organize cost reduction programmes with the help of different departmental, managers., q. To provide specialized services of cost audit in order to prevent the errors and frauds, and to facilitate prompt and reliable information to management., r. To find out costing profit or loss by identifying with revenues the costs of those, products or services by selling which the revenues have resulted., , Objectives of cost accounts, Following are the main objectives of cost accounting:, 1. To ascertain the cost per unit of the different products manufactured by a business concern;, 2. To provide a correct analysis of cost both by process or operations and by different, elements of cost;, 3. To disclose sources of wastage whether of material, time or expense or in the use of, machinery, equipment and tools and to prepare such reports which may be necessary to, control such wastage;, 4. To provide requisite data and serve as a guide for fixing prices of products manufactured, or services rendered;, 5. To ascertain the profitability of each of the products and advise management as to how, these profits can be maximised;, 6. To exercise effective control if stocks of raw materials, work-in-progress, consumable, stores and finished goods in order to minimise the capital locked up in these stocks;

Page 3 :

7. To reveal sources of economy by installing and implementing a system of cost control for, materials, labour and overheads;, 8. To advise management on future expansion policies and proposed capital projects;, 9. To present and interpret data for management planning, evaluation of performance and, control;, 10. To help in the preparation of budgets and implementation of budgetary control;, 11. To organise an effective information system so that different levels of management may, get the required information at the right time in right form for carrying out their individual, responsibilities in an efficient manner;, 12. To guide management in the formulation and implementation of incentive bonus plans, based on productivity and cost savings;, 13. To supply useful data to management for taking various financial decisions such as, introduction of new products, replacement of labour by machine etc.;, 14. To help in supervising the working of punched card accounting or data processing, through computers;, 15. To organise the internal audit system to ensure effective working of different, departments;, 16. . To organise cost reduction programmes with the help of different departmental, managers;, 17. To provide specialised services of cost audit in order to prevent the errors and frauds and, to facilitate prompt and reliable information to management; and, 18. To find out costing profit or loss by identifying with revenues the costs of those products, or services by selling which the revenues have resulted., , Advantages of Cost accounting, , 1 Disclosure of profitable and unprofitable activities, Since cost accounting minutely calculates the cost, selling price and profitability of product,, segregation of profitable or unprofitable items or activities becomes easy., , 2 Guidance for future production policies, On the basis of data provided by costing department about the cost of various processes and, activities as well as profit on it, it helps to plan the future.

Page 4 :

3 Periodical determination of profit and losses, Cost accounting helps us to determine the periodical profit and loss of a product., , 4 To find out exact cause of decrease or increase in profit, With the help of cost accounting, any organization can determine the exact cause of decrease, or increase in profit that may be due to higher cost of product, lower selling price or may be, due to unproductive activity or unused capacity., , 5 Control over material and supplies, Cost accounting teaches us to account for the cost of material and supplies according to, department, process, units of production, or services that provide us a control over material, and supplies., , 6 Relative efficiency of different workers, With the help of cost accounting, we may introduce suitable plan for wages, incentives, and, rewards for workers and employees of an organization., , 7 Reliable comparison, Cost accounting provides us reliable comparison of products and services within and outside, an organization with the products and services available in the market. It also helps to achieve, the lowest cost level of product with highest efficiency level of operations., , 8 Helpful to government, It helps the government in planning and policy making about import, export, industry and, taxation. It is helpful in assessment of excise, service tax and income tax, etc. It provides, readymade data to government in price fixing, price control, tariff protection, etc., , 9 Helpful to consumers, Reduction of price due to reduction in cost passes to customer ultimately. Cost accounting, builds confidence in customers about fairness of price., , 10 Classification and subdivision of cost, Cost accounting helps to classify the cost according to department, process, product, activity,, and service against financial accounting which give just consolidate net profit or loss figure, of any organization without any classification or sub-division of cost., , 11 To find out adequate selling price, In tough marketing conditions or in slump period, the costing helps to determine selling price, of the product at the optimum level, neither too high nor too low., , 12 Proper investment in inventory

Page 5 :

Shifting of dead stock items or slow moving items into fast moving items may help company, to invest in more proper and profitable inventory. It also helps us to maintain inventory at the, most optimum level in terms of investments as well as variety of the stock., , 13 Correct valuation of inventory, Cost accounting is an accurate and adequate valuation technique that helps an organization in, valuation of inventory in more reliable and exact way. On the other hand, valuation of, inventory merely depends on physical stock taking and valuation thereof, which is not a proper, and scientific method to follow., , 14 Decision on manufacturing or purchasing from outside, Costing data helps management to decide whether in-house production of any product will be, profitable, or it is feasible to purchase the product from outside. In turn, it is helpful for, management to avoid any heavy loss due to wrong decision., , 15 Reliable check on accounting, Cost accounting is more reliable and accurate system of accounting. It is helpful to check, results of financial accounting with the help of periodic reconciliation of cost accounts with, financial accounts., , 16 Budgeting, In cost accounting, various budgets are prepared and these budgets are very important tools, of costing. Budgets show the cost, revenue, profit, production capacity, and efficiency of plant, and machinery, as well as the efficiency of workers. Since the budget is planned in scientific, and systemic way, it helps to keep a positive check over misdirecting the activities of an, organization., , Differences between Financial Accounting and Cost Accounting, BASIS FOR, COMPARISON, Meaning, , COST ACCOUNTING, Cost Accounting is an, accounting system,, through which an, organization keeps the, track of various costs, incurred in the business, in production activities., , FINANCIAL ACCOUNTING, Financial Accounting is an, accounting system that, captures the records of, financial information about, the business to show the, correct financial position of, the company at a particular, date.

Page 6 :

Information type Records the information, related to material, labor, and overhead, which are, used in the production, process., , Records the information, which are in monetary, terms., , Which type of, cost is used for, recording?, , Both historical and predetermined cost, , Only historical cost., , Users, , Information provided by, the cost accounting is, used only by the internal, management of the, organization like, employees, directors,, managers, supervisors, etc., , Users of information, provided by the financial, accounting are internal and, external parties like, creditors, shareholders,, customers etc., , Valuation of, Stock, , At cost, , Cost or Net Realizable, Value, whichever is less., , Mandatory, , No, except for, manufacturing firms it is, mandatory., , Yes for all firms., , Time of, Reporting, , Details provided by cost, accounting are frequently, prepared and reported to, the management., , Financial statements are, reported at the end of the, accounting period, which is, normally 1 year., , Profit Analysis, , Generally, the profit is, analyzed for a particular, product, job, batch or, process., , Income, expenditure and, profit are analyzed together, for a particular period of the, whole entity., , Purpose, , Reducing and controlling, costs., , Keeping complete record of, the financial transactions., , Forecasting, , Forecasting is possible, through budgeting, techniques., , Forecasting is not at all, possible.

Page 7 :

The difference between management and cost accounting are as, follows, .No., , Cost Accounting, , Management Accounting, , 1, , The main objective of cost, accounting is to assist the, management in cost control and, decision-making., , The primary objective of management accounting, is to provide necessary information to the, management in the process of its planning,, controlling, and performance evaluation, and, decision-making., , 2, , Cost accounting system uses, quantitative cost data that can, be measured in monitory terms., , Management accounting uses both quantitative, and qualitative data. It also uses those data that, cannot be measured in terms of money., , 3, , Determination of cost and cost, control are the primary roles of, cost accounting., , Efficient and effective performance of a concern, is the primary role of management accounting., , 4, , Success of cost accounting, does not depend upon, management accounting, system., , Success of management accounting depends on, sound financial accounting system and cost, accounting systems of a concern., , 5, , Cost-related data as obtained, from financial accounting is the, base of cost accounting., , Management accounting is based on the data as, received from financial accounting and cost, accounting., , 6, , Provides future cost-related, decisions based on the historical, cost information., , Provides historical and predictive information for, future decision-making., , 7, , Cost accounting reports are, useful to the management as, well as the shareholders and, creditors of a concern., , Management accounting prepares reports, exclusively meant for the management., , 8, , Only cost accounting principles, are used in it., , Principals of cost accounting and financial, accounting are used in management accounting.

Page 8 :

9, , Statutory audit of cost, accounting reports are, necessary in some cases,, especially big business houses., , No statutory requirement of audit for reports., , 10, , Cost accounting is restricted to, cost-related data., , Management accounting uses financial, accounting data as well as cost accounting data., , Elements of Cost, Mere knowledge of total cost cannot satisfy the needs of management. For proper, control and managerial decisions, management is to be provided with necessary data to analyse, and classify costs. For this purpose, the total cost is analysed by elements of cost. i.e. by the, nature of expenses. Strictly speaking, the elements of cost are three i.e., materials, labour and, other expenses. These elements of cost are further analysed into different elements as illustrated, in the following charts:, , By grouping the above elements of cost, the following divisions of cost are obtained :, 1. Prime Cost, = Direct Material + Direct Labour., 2. Works of Factory Cost, = Prime Cost + Works or Factory Overheads, 3. Cost of Production, = Works Cost + Administration overheads, 4. Total Cost or Cost of Sales, =Cost of Production + Selling and Distribution, Overheads., Classification of cost, Cost classification is the process of grouping costs according to their common, characteristics. It is the placement of like items together according to their common, characteristics. A suitable classification of costs is of vital importance in order to identify the, cost with cost centre or cost units. Cost may be classified according to their nature i.e., material,, labour and expenses and a number of other characteristics. The same cost figures are classified, according to different ways of costing depending upon the purpose to be achieved and, requirements of a particular concern. The important ways classification are:

Page 9 :

1. By Nature or Elements, 2. By Functions, 3. By Degree of traceability to the product, 4. By Changes in Activity or Volume, 5. By Controllability, 6. By Normality, 7. By Relationship with Accounting period. (Capital and Revenue), 8. By Time, 9. According to Planning and Control, 10.By Association with the product, 11. For Managerial Decisions., Now each classification will be discussed in details., 1. By Nature or elements, or analytical Classification : According to this classification,, the costs are divided into three categories i.e. Materials, Labour and expenses. There, can be further sub – classification of each elements. For example: material into raw, material components, spare parts, consumable stores, packing material etc. This, classification is important as it helps to find out the total cost, how such total cost is, constituted and valuation of work-in –progress., 2. By functions (i.e, Functional Classification). According to this classification costs, are divided in the lights of the different aspects of basic managerial activities involved, in the operation of a business undertaking. It leads to grouping of cost according to the, broad divisions of functions of a business undertaking i.e. production, administration,, selling and distribution. According to this classification costs are divided as follows., Manufacturing and production Coast. This is the total of costs involved in, manufacture, construction and fabrication of units of production., Commercial Cost. This is the total of costs incurred in the operation of business, undertaking other than the cost of manufacturing and production. Commercial cost may

Page 10 :

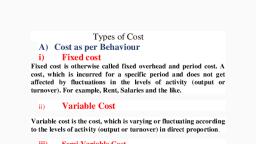

further be sub – divided into (a) administrative cost, and (b) selling and distribution, cost. These terms will be explained in a subsequent chapter., 3. By degree of Traceability to the Product (Direct and Indirect). According to this, classification, total cost is divided into direct costs and indirect costs. Direct costs are, those which are incurred for and may be conveniently identified with a particular cost, centre or cost unit . Material used and labour employed in manufacturing as article or, n a particular process of production are common examples of direct costs. Indirect costs, are those costs which are incurred for the benefits of a number of cost centres or cost, units and cannot be conveniently identified with a particular cost centre of cost unit., 4. By Changes in Activity or volume. According to this classification, costs are classified, according to their behaviour in relation to changes in the level of activity or volume of, production. On this basis, costs are classified into three groups viz., fixed variable and, semi-variable., (i), , Fixed Costs are commonly described as those which remain fixed in total amount, with increase or decrease in the volume of output or productive activity for a given, period of time. Fixed cost per unit decreases as production increases and increases, production declines. Examples of fixed costs are rent. Insurance of factory building,, factory manager’s salary etc., , Fixed costs can be classified into following categories :, (a) Committed Costs. These costs are the result of inevitable consequences of, commitments previously made or are incurred to maintain certain facilities and cannot, be quickly eliminated. The management has title or no discretion in such of costs e.g., rent, insurance, depreciation on building or equipment purchased, (b) Policy and managed Costs. Policy Costs are incurred for implementing some, management policies as executive development, housing etc. and are often, discretionary, Managed Costs are incurred to ensure the operating existence of the, company e.g. staff services., (c) Discretionary Costs. These costs are not related to the operation by can be controlled, by the management. These costs arise from some policy decisions, new researches etc., and can be eliminated or reduced to a describe level at the discretion of the, management., (d) Step Costs. Such costs are constant for a given level of output and then increase by a, fixed amount at a higher level of output., (ii), (iii), , Variable Costs are those which vary in total in direct proportion to the volume of, output, These costs per unit remain relatively constant with changes in production., Semi –variable Costs are those which are partly fixed and partly variable, for, examples, telephone expenses include a fixed portion of annual charges plus, variable according to calls: thus total telephone expenses are semi-variable. Other

Page 11 :

examples of such costs are depreciation, repairs and maintenance of building and, plants etc., 5. By Controllability. Under this, costs are classified according to whether or not they, are influenced by the action of a given member of the undertaking. On this basic cost, it classified into two categories., (i), Controllable costs are those which can be influenced by the action of a, specified member of an undertaking., (ii), Uncontrollable costs are those which cannot be influenced by the action of, a specified member of an undertaking., 6. By Normality : Under this, costs are classified according to whether these are costs, which are normally incurred at a given level of output in the conditions in which that, level of activity is normally attained. On this basis, it is classified into two categories., (a) Normal cost. It is the cost which is normally incurred at a given level of output in, the conditions in which that levels of output is normally attained. It is part of cost of, production., (b) Abnormal cost. It is the cost which is not normally incurred at a given level of output, in the conditions in which that level of output us normally. It is nor a part of cost of, production and charged of Costing Profit and Loss Account., 7. By Relationship with Accounting Period (Capital and Revenue) The cost which is, incurred in purchasing assets either to earn income or increasing the earning capacity, of the business is called capital cost.’, 8. By Time. Costs can be classified as (i) Historical costs and (ii) Predetermined costs., (i), Historical Costs. The costs are ascertained after being incurred are called, historical costs., (ii), Predetermined Costs. Such costs are estimated costs i.e. computed in, advance of production., 9. According to planning and control. Planning and control are two important functions, of management. Cost accounting furnishes information to the management which is, helpful in the due discharge of these two functions. According to this, costs can be, classified as budgeted costs and standard costs., (i), Budgeted Costs: Budgeted cost represent an estimate of expenditure for, different phases of business operations such as manufacturing,, administration, sales, research and development etc., (ii), Standard Costs: Budgeted cost are translated in actual operation through, the instrument of standard costs., 10. By Association with the product. Under this classification, cost can be product costs, and period costs.Products costs are those costs which are traceable to the product and, are include in inventory valuation. It comprises direct materials, direct labour and

Page 12 :

manufacturing overheads in case of manufacturing concerns. Period costs are incurred, on the basis of time such as rent, salaries etc., , Limitations of Cost Accounting, Limitations of Cost Accounting – Cost Accounting is Unnecessary, Cannot be Adopted, by Small Business Concerns, Very Costly and Results are Misleading, , , , , , Cost Accounting is Unnecessary: ..., Cost Accounting System cannot be adopted by Small Business Concerns: ..., Cost Accounting System is Very Costly: ..., Costing Results are Misleading: