Page 1 :

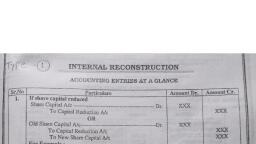

358 Holding Company Accounts, Working Note, , 1. Control Chart: Items from the Balance Sheet of § Lid., { Majority 0% s, cs ac AA ea, , it, Rs. Mea | Cost of pP&Lof, Marked items of 5 Lid. : of, , control H. Ld., v Dp wu 20, ,, Share Ca ital 1,00 000 0,000 20,000, , General Reserve as per B/8 30,000, b Poe Loss “A/c 10,000,, (40,000 ), Breseik g 5 ‘ } 35,000 . 7,000 28,000, ce a 5,000 1,000 =, , Iitustration 5 [ Capital Reserve - Revaluation of Assets ], From the Balance Sheets giver below, prepare 4 Consolidated Balance Sheet., , Balance Sheets as at 3ist December, 1987, , : : H. Ltd. | 5 Led. Assets, ee Liabilities ee ee , Share Capital :, ~ Shares of Rs., , Fixed Assets, 10 each i x 2,000 Stock, , The followiug information is available :, , (1) The entire profit of S Ltd., - has been earned since th, © shares were acquired, , b, y H Ltd, but there was already the reserve of Rs. 600 at that date., (2), , Bills accepted by S Ltd. are all in f,, Rs. 400 of them. avour of H Ltd. which had discounted, , Fixed assets of S Ltd. are under-valued by Rs. 200 4, , The stock of H Ltd. includes Bs. 5, p 00 for goods bought from S$ Ltd, at a, , 5 profit to the latter of 25 per cent on cost. os, t. \Soldiion ae, , as, , _-A pencil. :, Yes, take a pencil and make two changes in the giv, , { By, Consolidated Balance Sheet of MH Ltd. and its Subsidiary S Ltd, As at 3lst December, 1987, , Liabilities, Share Capital : Fixed Assets, 1,000 Shares of, Rs 10 cach 10,000 | Stock §,500, Capital Reterve - Less Unirealised profit 100, omcont, ( from contra } aun Debtors, Reserve 1,000, '\ Bills Receivable 100, Less Inter-co. bills 100, , Assets, , aa, , Profit and Loss Afc 4,000, Add Post-acqi. profit 900, , 4,900 “Cost of Control (3/4), Less Unrealised Purchase’price of, profit on stock 100 shares 1,500, ‘. : Less —, Creditors 7 EP vine value 1,500, Bills Payable 500 Reserve 450, , Less Inter-co. bills 100 Profit on revaluation 150, Minority ( 1/4) ene Capital Reserve —600, Share Capital 500 to contra, Reserve 150, Post-acqui. profit 300, Profit on revalution 50, , é ; en balance sheet of S, Ltd. Aad Rs. 200 to its fixed assets. This is profit. Put it on its liability oe, ‘ é \ (, , Ors, , AU, , AW, , A, Sif Ef, , 8, m, , te, ag, , Ni, x