Page 1 :

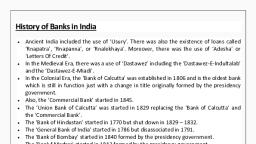

History of Banking in India –, History of Banking in India (Before & After Independence): The banking system is considered as, the backbone of a nation's economy. Modern banking in India originated in the last decade of the 18th, century. We have come up with the history of banking, before and after independence., The history of banking began when empires needed a way to pay for foreign goods and services with, something that could be exchanged or facilitated easily. Prior to this, banking procedures were carried by, informal methods in the ancient World. However, formal banking has been developed around the 20th, century. In India, banking has developed from the primitive to the modern stage of banking in a fashion that, has no parallel in world history., In India, references about banking and regulations were even found in our scriptures and ancient texts., Banking products are also found quoted in Chanakya’s Arthashastra (300 B.C.).Moving to Modern day, banking system, the concept of banking is laid by the people of Italy under the name Banco., Banking in India forms the base for the economic development of the country. Major changes in the, banking system and management have been seen over the years with the advancement in technology,, considering the needs of people., The banking sector development can be divided into three phases:, Phase I: The Early Phase which lasted from 1770 to 1969, Phase II: The Nationalisation Phase which lasted from 1969 to 1991, Phase III: The Liberalisation or the Banking Sector Reforms Phase which began in 1991 and continues to, flourish till date, Given below is a pictorial representation of the evolution of the Indian banking system over the years:, , The advancement in the Indian banking system is classified into 3 distinct phases:, 1. The pre-independence phase i.e. before 1947., 2. Second phase from 1947 to 1991., 3. Third phase 1991 and beyond., , Pre Independence Period (1786-1947) –, The first bank of India was the “Bank of Hindustan”, established in 1770 and located in the then Indian, capital, Calcutta. However, this bank failed to work and ceased operations in 1832. The General Bank of, India, established in 1786 but failed in 1791., During the Pre Independence period over 600 banks had been registered in the country, but only a few, managed to survive., 1|Page

Page 2 :

Following the path of Bank of Hindustan, various other banks were established in India. They were:, , , , , , , , The General Bank of India (1786-1791), Oudh Commercial Bank (1881-1958), Bank of Bengal (1809), Bank of Bombay (1840), Bank of Madras (1843), During the British rule in India, The East India Company had established three banks: Bank of, Bengal, Bank of Bombay and Bank of Madras and called them the Presidential Banks. These three, banks were later merged into one single bank in 1921, which was called the “Imperial Bank of, India.”, , , , The Imperial Bank of India was later nationalised in 1955 and was named The State Bank of India,, which is currently the largest Public sector Bank. For many years, the presidency banks had acted, as quasi-central banks, as did their successors, until the Reserve Bank of India was established., , , , In April 1935, Reserve Bank of India was formed based on the recommendation of Hilton Young, Commission (setup in 1926)., , , , In this time period, most of the bank were small in size and suffered from high rate of failures. As a, result public confidence is low in these banks and deposit mobilization was also very slow. People, continued to rely on unorganized sector (moneylenders and indigenous bankers)., , Given below is a list of other banks which were established during the Pre-Independence period:, , Bank Name, , Year of Establishment, , Allahabad Bank, , 1865, , Punjab National Bank, , 1894, , Bank of India, , 1906, , Central Bank of India, , 1911, , Canara Bank, , 1906, , Bank of Baroda, , 1908, , If we talk of the reasons as to why many major banks failed to survive during the pre-independence period,, the following conclusions can be drawn:, , , , , , , Indian account holders had become fraud-prone, Lack of machines and technology, Human errors & time-consuming, Fewer facilities, Lack of proper management skills, , Following the Pre-Independence period was the post-independence period, which observed some, significant changes in the banking industry scenario and has till date developed a lot., , 2|Page

Page 3 :

Post Independence Period (1947-1991) –, At the time when India got independence, all the major banks of the country were led privately which was a, cause of concern as the people belonging to rural areas were still dependent on money lenders for financial, assistance., With an aim to solve this problem, the then Government decided to nationalise the Banks. These banks, were nationalised under the Banking Regulation Act, 1949. Whereas, the Reserve Bank of India was, nationalised in 1st January, 1949., Need for nationalization in India:, a) The banks mostly catered to the needs of large industries, big business houses., b) Sectors such as agriculture, small scale industries and exports were lagging behind., c) The poor masses continued to be exploited by the moneylenders., Following it was the formation of State Bank of India in 1955 and the other 14 banks were nationalised, between the time duration of 1969 to 1991 under the regime of Smt. Indira Ganndhi being the Prime, Minister. These were the banks whose national deposits were more than 50 crores., Given below is the list of these 14 Banks nationalised in 1969:, 1. Allahabad Bank, 2. Bank of India, 3. Bank of Baroda, 4. Bank of Maharashtra, 5. Central Bank of India, 6. Canara Bank, 7. Dena Bank, 8. Indian Overseas Bank, 9. Indian Bank, 10. Punjab National Bank, 11. Syndicate Bank, 12. Union Bank of India, 13. United Bank, 14. UCO Bank, In the year 1980, another 6 banks were nationalised, taking the number to 20 banks. These banks, included:, 1., 2., 3., 4., 5., 6., , Andhra Bank, Corporation Bank, New Bank of India, Oriental Bank of Comm., Punjab & Sind Bank, Vijaya Bank, , Apart from the above mentioned 20 banks, there were seven subsidiaries of SBI which were nationalised in, 1959:, 1., 2., 3., 4., 5., 6., 7., , State Bank of Patiala, State Bank of Hyderabad, State Bank of Bikaner & Jaipur, State Bank of Mysore, State Bank of Travancore, State Bank of Saurashtra, State Bank of Indore, , 3|Page

Page 4 :

All these banks were later merged with the State Bank of India in 2017, except for the State Bank of, Saurashtra, which merged in 2008 and State Bank of Indore, which merged in 2010., Meanwhile on the recommendation of M.Narsimhan committee, RRBs (Regional Rural Banks) were formed, on Oct 2, 1975. The objective behind the formation of RRBs was to serve large unserved population of rural, areas and promoting financial inclusion., With a view to meet the specific requirement from the different sector (i.e. agriculture, housing, foreign, trade, industry) some apex level banking institutions were also setup like, 1. NABARD (est. 1982), 2. EXIM (est. 1982), 3. NHB (est. 1988), 4. SIDBI (est. 1990), In 1993, New Bank of India got merged with Punjab National Bank., , Impact of Nationalisation –, There were various reasons why the Government chose to nationalise the banks. Given below is the, impact of Nationalising Banks in India:, , , This lead to an increase in funds and thereby increasing the economic condition of the country, Increased efficiency, Helped in boosting the rural and agricultural sector of the country, It opened up a major employment opportunity for the people, The Government used profit gained by Banks for the betterment of the people, The competition decreased, which resulted in increased work efficiency, This post Independence phase was the one that led to major developments in the banking sector of India, and also in the evolution of the banking sector., , Liberalisation Period (1991-Till Date) –, Once the banks were established in the country, regular monitoring and regulations need to be followed to, continue the profits provided by the banking sector. The last phase or the ongoing phase of the banking, sector development plays a hugely significant role., This period saw a remarkable growth in the process of development of banks with the liberalization of, economic policies. Even after nationalization and the subsequent regulations that followed, a large portion, of masses are untouched by the banking services., To provide stability and profitability to the Nationalised Public sector Banks, the Government decided to set, up a committee under the leadership of Shri. M Narasimham to manage the various reforms in the Indian, banking industry., Considering this, in 1991, the Narsimhan committee gave its recommendation. The biggest development, was the introduction of Private sector banks in India. RBI gave license to 10 Private sector banks to, establish themselves in the country out of which only 6 private banks survived. These banks included:, 1., 2., 3., 4., 5., 6., 7., 8., , Global Trust Bank, ICICI Bank, HDFC Bank, Axis Bank, Bank of Punjab, IndusInd Bank, Centurion Bank, IDBI Bank, 4|Page

Page 5 :

9. Times Bank, 10. Development Credit Bank (DCB), In 1998, the Narsimhan committee again recommended entry of more private players. As a result RBI gave, license to, 1. Kotak Mahindra Bank (2003), 2. Yes Bank (2004), In 2013-14, 3rd round of bank licensing took place. And in 2014 IDFC bank and Bandhan Bank emerged., In order to further financial inclusion, RBI also proposed to set up 2 kind of banks i.e, Payment Banks and, Small Banks., The other measures taken include:, , , , , , , , , Setting up of branches of the various Foreign Banks in India., No more nationalisation of Banks could be done., The committee announced that RBI and Government would treat both public and private sector, banks equally., Any Foreign Bank could start joint ventures with Indian Banks., Payments banks were introduced with the development in the field of banking and technology., Small Finance Banks were allowed to set their branches across India., A major part of Indian banking moved online with internet banking and apps available for fund, transfer., , Conclusion –, Thus, the history of banking in India shows that with time and the needs of people, major developments, have been brought about in the banking sector with an aim to prosper it., The entire period of evolution of the banking industry is ongoing, and each day new changes can be seen, in the banking sector for the betterment of the economic growth of the country., , *****, , 5|Page