Notes of B.Com.III 2021-22, Taxation Bcom-lll Tax.pptx - Study Material

Page 1 :

B.COM-III ADVANCED ACCOUNTANCY-IV (Taxation), Wef. June 2020-21, Module-I, Definition, Residence and Tax liability

Page 2 :

INCOME TAX ACT 1961:�DEFINITIONS-, Person, Assessee, Assessment, Assessment Year & Previous Year, Income, Gross Total Income, Agricultural Income, Company, Indian company

Page 3 :

Person-, An Individual- natural human beings includes minors and insane eg. Rohan, Sushila, Mr. Goyal etc., A Hindu Undivided Family (HUF)- joint Hindu family but not joint family of Christians or Muslims. Eg. Joint hindu family of Mr. Jain, Joint hindu family of Kulkarni etc., Firm- partnership concern governed by Partnership Act 1932 eg. M/s Shaha and Mehta Associates, M/s Sawant and brothers associates etc., A Company- Indian company or foreign company as defined u/s 2(17) eg. Parishwad & sons Pvt Ltd., Tata Finance Co. Ltd. etc, An Association of Person (AOP)- refers to a body of persons, whether incorporated or not, who have joined together to serve common interest eg. Trade unions, Indian Medical associations, Trusts and cooperative societies etc., A Local Authority- local self governing bodies eg. Municipalities, gram panchayats, municipal corporations, district boards etc., Every Artificial Juridical Person- all remaining entities not covered under above six categories eg. Deity, idols, pubic corporations established under special act- Shivaji University, Mahalaxmi mandir etc.

Page 4 :

Assessee-, An assessee is a person:, From whom any tax is payable under the act., From whom any other sum of money (such as interest or penalty) is payable under the act., Against whom any proceedings under the act have been initiated for the assessment of his income or loss or of amount of refund due to him., Who is deemed to be an assessee i.e. representative assessee such as guardian of minor or manager of a lunatic or agent of a non-resident., Who is deemed to be an assessee in default i.e. a person who has failed to discharge any obligation under the act e.g. deduction of tax at source, payment of advance tax etc. , In short, assessee is a person by whom tax or any other sum of money is payable or any deemed assessee liable to pay tax on other’s income under this act. The other sum of money includes fine, penalty and interest.

Page 5 :

Assessment-, Assessment consists of two stages:, Computation of total income of assessee according to the Income Tax Act 1961., Determination of tax liability on such income according to the Finance Act of the relevant year., Income-, Definition of income under Income Tax Act, is inclusive and includes:, Profits and gains, Dividends, Charity received to trust, Remuneration, Allowances other than salary, Perquisites provided, Daily allowance to directors, Profit from insurance business, Any casual receipts, Profit from keyman insurance policy, Any gift in excess of Rs. 50000 at a time, Profits on sale of a license granted, Interest, salary, bonus, commission or remuneration received by the partner from the firm.

Page 6 :

Assessment Year & Previous Year-, Assessment Year (A.Y.)-, Assessment year means the period of twelve months commencing on the first day of April every year and ending on thirty first March of the subsequent year. It is also called Tax Year, Government Year, Financial year, or Fiscal year. The total income of a person and his tax liability is accesses in the A.Y. as per provisions applicable to that year., Previous Year (P.Y.)-, Previous year means the financial year immediately preceding the Assessment year. The income of the previous year is assessed to tax in the assessment year. It is also called ‘Income earning year’, year of account or accounting year of income. The previous year starts from 1st April and concludes on 31st March every year. In case of newly set up business or profession, the first previous year will be the period commencing from the date of setting up of the business or profession and ending on immediately following 31st March. , E.g. If a newly set up business is on 15th Sept. 2015, the P.Y. is 15-09-2015 to 31-03-2016 and A.Y. is 2016-17. thus for the P.Y. 2020-21 (1st April, 2020 to 31st March, 2021) A.Y. is 2021-2022 (1st April, 2021 to 31st March, 2022).

Page 7 :

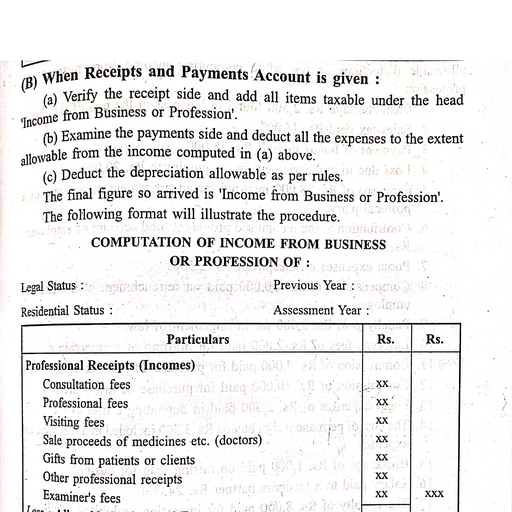

Gross Total Income-, Gross Total Income means the total income computed in accordance with the provisions of the Income Tax Act before making any deduction under section 80 C to 80 U or u/s 280-U. Under the Income Tax Act, various types of income liable to the tax have been classified under five heads and total of these heads is Gross Total Income-, , Income from Salaries xxx, Income from House Property xxx, Profits and Gains from business or profession xxx, Capital gain xxx, Income from other sources xxx, -----, GROSS TOTAL INCOME: xxx

Page 8 :

Total Income or Taxable Income-

Page 9 :

Agricultural Income-, In India Agricultural Income is total exempted u/s 10 (1). Definition of Agricultural Income includes:, Any amount or revenue derived from land., Any income from process which make prouse marketable., Any income from farm house., here any income derived from land is agricultural income if fulfil following three conditions-, Income derived from land , Land must be situated in India, Agricultural activities must be carried on it., Prouse means raw crop. Any process carried on for making prouse marketable is agricultural activity and income derived from it is agricultural income., Any house become farm house if following three conditions are satisfied-, House must be immediately vicinity of agricultural land., House is used for dwelling or storing of material., House is not within 8 km from urban area.

Page 10 :

Residential status and tax lability-, Income tax liability of an assessee depends upon his residential status., -Types of Residential Status-, On the basis of residence, all the assessee are classified into two classes:, Residence of India (ROI), Non-residence of India (NRI), Resident in India category is further classified into two types (only for individuals and HUFs):, Resident and Ordinary Resident (ROR), Resident but not Ordinary Resident (RNOR)

Page 11 :

A person can be classified on the basis of residential status in the following manner:, Person (Assessee), , , , , , An Individual and HUF can be –, Resident and Ordinarily Resident (Resident) (R), Resident but Not Ordinarily Resident (Not Ordinarily Resident) (NOR), Non-Resident (NR), Other entities in person can be-, Resident (R) or, Non-Resident (NR), Resident and Ordinarily Resident but not Ordinarily Resident (ROR) Resident (RNOR) , (For Individuals & HUF only), Resident (R) Non Resident (NR)

Page 12 :

COMPUTATION OF INCOME FROM SALARY , Legal status: Individual P.Y.-2019-20, Residential status: Resident A.Y.- 2020-21

Page 13 :

PARTICULARS, AMOUNT, AMOUNT

Learn better on this topic

Learn better on this topic