Notes of AAO CLASS, Service Rules & LDCE & AAO Bank-Reconciliation-State - Study Material

Page 1 :

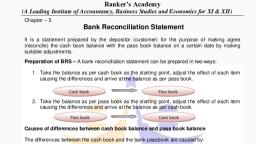

Bank Reconciliation Statement, What is Bank Reconciliation Statement?, Bank reconciliation statement is a financial statement prepared to reconcile the, differences in the balance of the bank column of cashbook and passbook by showing all, the causes of difference between the two., , Bank Reconciliation Statement Examples, ● A cheque of INR 3 lakhs was not collected by the bank but was deposited, ● Rs. 2500 was charged by the bank and recorded in the passbook but not in the, company’s cash book, ● The interest of Rs. 2000 was credited by the bank but not recorded in the cash, book, , Recording of Transactions in Cashbook and Passbook, When the money is deposited in the bank, firms enter the transaction on the debit side, of the bank column of the cashbook, and at the same time, the bank also counts the, same transaction on the credit side of the firm’s accounts maintained with it. On the, other hand, when the money is withdrawn from the bank, firms enter the transaction on, the credit side of the cashbook. At the same time, the bank enters the transaction on the, debit side of the firm’s account with it or in the passbook., Therefore, all the entries recorded on the debit side of the bank column of the cashbook, must tally with the entries noted on the credit side of the passbook with the bank. In the, same way, all the entries recorded on the credit side of the cashbook must tally with the, entries recorded on the debit side of the passbook. Hence, all the entries recorded on, the cashbook and passbook must match with each other at any point in time., , Process of Balancing Cashbook and Passbook

Page 2 :

One of the most vital distinctions that students of class 11 studying bank reconciliation, statements must be through with is that of cashbook and passbook. Both the terms, have their significant meaning under this topic. Let us have a look at their differences● The cheque is issued to the creditor by the firm and recorded on the credit side of, the cashbook. The cheque, however, is presented to the bank after some days., Due to this reason, entries made in the passbook have a time gap with the entry, of the cash book, ● There is a subsequent time gap throughout the process- such as the day when, the firm receives the cheque from the customer, and the firm deposits the cheque, to the bank for collection. And, also between the bank making an entry on the, debit side of the cash book and recording it on the credit side of the passbook, ● When the cheque is received from some other party, it is deposited with the bank,, and the entry is made on the cashbook. But, if it is dishonoured, then the bank, will not make any entry in the passbook, ● Sometimes, customers make overdrafts and bank charges interest on it, or there, are bank charges and commission charged by the bank from time to time, and, the bank debit the firm’s account with it, but the entry in the passbook is made, only when the statement is received from the bank, ● Banks also collect dividends and interest on customer investment and credit the, firm’s account with it or passbook. Still, the customer makes the entry in the, cashbook after they receive the statement of the passbook from the bank, , Importance of Bank Reconciliation Statements, As the chapter 5th of class 11 accountancy aims to create a solid foundation for the, upcoming topics, it is necessary to understand this one in depth. Here are some, simplified pointers that will help you understand the importance of bank reconciliation, statements● A bank reconciliation statement shows errors made in both the books by, customers or banks and helps to rectify it, ● It helps in making future transactions secure with the bank if the customer is sure, about the correctness of balance in the cash book, ● It helps in preparing the revised cash book as entries like bank charges, interest, allowed or charged by the bank, etc. are recorded in the passbook and will be, recorded in the cashbook in the future, ● Any fraud made by the bank or any other party can be disclosed through it. For, Example: If any staff shows any type of deposit in the bank but it is actually not, deposited, then it can be disclosed easily with the help of this statement

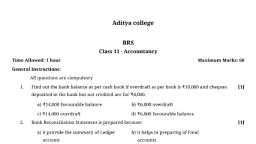

Page 3 :

● According to the chapter, it helps in keeping track of cheque sent to the bank for, collection and reveals the delay in the collection of cheque by the bank, , Steps to Prepare Bank Reconciliation Statements, A bank reconciliation statement is prepared when customers or firms get their passbook, updated from the bank. The customers or firms then tally the entries and balance of, both cashbook and passbook. Following steps are required to prepare the bank, reconciliation statements:, Step 1: Tick the items on the debit side of the cashbook which tally with the items on the, credit side of the passbook, and note down the unticked items, which is the cause of the, difference in balances of both the books, Step 2: In the same way, tick the items on the credit side of the cash book, which tally, with the items on the debit side of the passbook and note down the unticked items, which do not tally in both the books, which is the cause of the difference, Step 3: Now a bank reconciliation statement can be prepared by taking the balance as, per the cash book as a starting point. If the statement is started with the bank column of, the cashbook, then the answer arrived will be the balance as per the passbook. Then,, you can add the items which have the effect of higher balance in the passbook and, deduct the items which influence lower balance in the passbook., Now that you are through with the process and steps of bank reconciliation statements,, let us go through the pointers which elaborate the entries which can be made in the, cashbook or passbook., , How to become a Chartered Accountant?, Balance as per cashbook can either be credit or debit:, ● Class 11 accountancy chapter bank reconciliation statements mention that the, Credit balance as per cash book shows the amount which has been withdrawn, more than deposit and credit balance as per cash book is also known as, ‘overdraft balance as per cash book’, ● Debit balance as per cash book shows that the firm or customer has so much, balance of deposit in the bank, , Balance as per passbook can be either credit or debit:, ● Credit balance as per passbook shows that the firm or customer has a given, amount in balance of deposit in the bank

Page 4 :

● Debit balance as per passbook shows the amount which has been withdrawn, more than the deposit and debits balance as per passbook is also known as, ‘overdraft balance as per passbook’, , Bank reconciliation Statement Rules, Rules help in avoiding any mistake in the statement. These rules act as a basic, framework for the statement. Here are some of the bank reconciliation statement rules:, 1. Any debit balance in the cash book is referred to as the deposits of the business, entity, 2. Debit in cash book is equal to credit in passbook, 3. Credit balance in cash book means unfavorable balance, 4. Debit balance in cash book means favorable balance, 5. Cheques that are issued but in any case not presented are adjusted in the cash, book, , Bank Reconciliation Statement Questions and Answers, Who is responsible for preparing the bank reconciliation statement?, A bank reconciliation statement is prepared by business organizations., What is the Bank reconciliation statement definition?, A bank reconciliation statement is a financial statement prepared to reconcile the, differences in the balance of the bank column of cashbook and passbook by showing all, the causes of difference between the two., Is a bank reconciliation statement a comparison report with a bank statement?, A bank reconciliation statement compares a bank statement with the balance of the, company’s accounts with the balance in the bank statement.

Learn better on this topic

Learn better on this topic